Budgeting is one of the most important milestones on the way to living a stress- and worry-free life, but some budgets can make you feel like you don’t have any money left over to actually enjoy.

If you’ve experienced any of these problems, then the 60-20-20 budget is perfect for you. It’s a budgeting template that lets you organize your finances in a simple way. The best part is that it actually leaves you some money to spend on yourself.

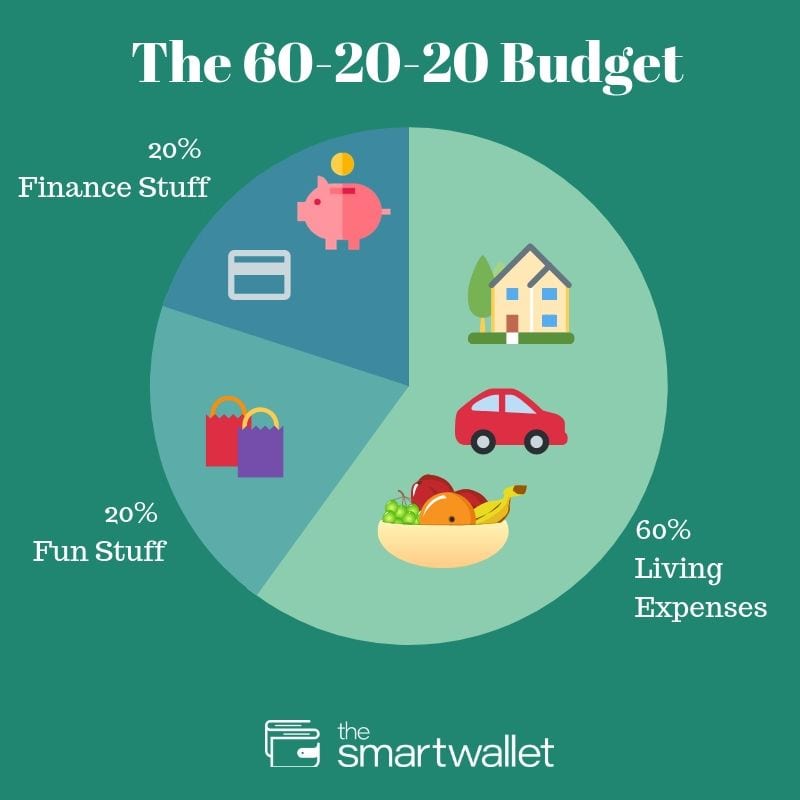

How the 60-20-20 Budget Works

The 60-20-20 budget works by allocating:

60% of your income to living expenses.

This includes everything from groceries and rent to mortgage, insurance payments and bills. You can think of this as “flow money” – it’s the money that flows into and out of your checking account every month.

20% of your income to strictly financial matters.

This includes servicing your debts, making deposits into your emergency fund, and of course, investments. You can fill these items in the same order as they are listed. After paying off your debts, you should focus on having enough money in your emergency funds to protect you from unforeseen circumstances. Beyond that, all your extra money should go into investments.

20% of your income to discretionary spending, or fun.

This includes things like eating out, going on dates, buying new clothes, and so on. You, however, have to ensure that you keep this segment at or below 20% because reports show that people tend to disregard their budgets when it comes to discretionary spending. Americans spend $1,497 per month (almost $18,000 a year) on non-essential items, but they still say they don’t have enough to put away for retirement.

The great thing about the 60-20-20 budget is that it already ensures that you don’t lose momentum and blow all your allocated funds. Statistics show that consumer debts are on the rise. Having a budget that makes you pay off your debts as quickly as possible is bound to keep you motivated.

How to Get Started

Working with the 60-20-20 budget is quite easy to do. All you really need is a pen and a piece of paper. You can write down your basic income and divide it into ten equal parts: Six go into your living expenses, two to your financial matters, and the remaining two parts to your discretionary spending.

You can also get another piece of paper and write out all your living expenses to see how much you need to cover them. Just writing these things out can help you identify where all your money is going and how you can allocate it better, even if you end up not following the budget to the letter.

Be Aware of Your Spending

You should know that this budget is more suitable for certain incomes than others. For example, if you earn a million dollars every year (extreme example, I know), it’s unlikely that your living expenses will cost up to 60% of that amount.

Additionally, your discretionary spending may not strictly fit into the 20% of your income. A smart decision is to get as much money as you can into investments and your emergency fund. You can then spend the returns on discretionary items. Like every budget, the point of 60-20-20 is to make you think about “discretionary” purchases before you make them. It takes out some of the spontaneous fun of discretionary items, but it also puts more money in your pocket in case of emergencies and for retirement.

In the same vein, the 60-20-20 budget may not apply to someone who has a lot of debt to pay down or who doesn’t have enough income. It’s unlikely that you’re going to spend 20% of your income on fun when you’d rather handle living expenses and bills. Most of it is probably going to your living expenses.

The 60-20-20 budget is not cast in stone, and you can modify various parts of it to fit your situation, as there are other budget solutions, like the 50-30-20 budget. The point is to find a way to distribute your income that meets your financial and emotional needs.

Don’t wait to get out of debt! Read this: A Complete, Step-By-Step Guide to Get Out of Debt.

Budgeting is one of the most important milestones on the way to living a stress- and worry-free life, but some budgets can make you feel like you don’t have any money left over to actually enjoy.

If you’ve experienced any of these problems, then the 60-20-20 budget is perfect for you. It’s a budgeting template that lets you organize your finances in a simple way. The best part is that it actually leaves you some money to spend on yourself.

Budgeting is one of the most important milestones on the way to living a stress- and worry-free life, but some budgets can make you feel like you don’t have any money left over to actually enjoy.

If you’ve experienced any of these problems, then the 60-20-20 budget is perfect for you. It’s a budgeting template that lets you organize your finances in a simple way. The best part is that it actually leaves you some money to spend on yourself.